Paper Planes

Will they soar high in the next cycle as well ?

Cyclical industries reward investors who know how to do one thing well: buy in bad times and sell in good times. Unlike complex restructuring or legal special situations, this is the simplest form of Special Situation investing — and, importantly, the one with the highest probability of making money for retail investors if executed with discipline.

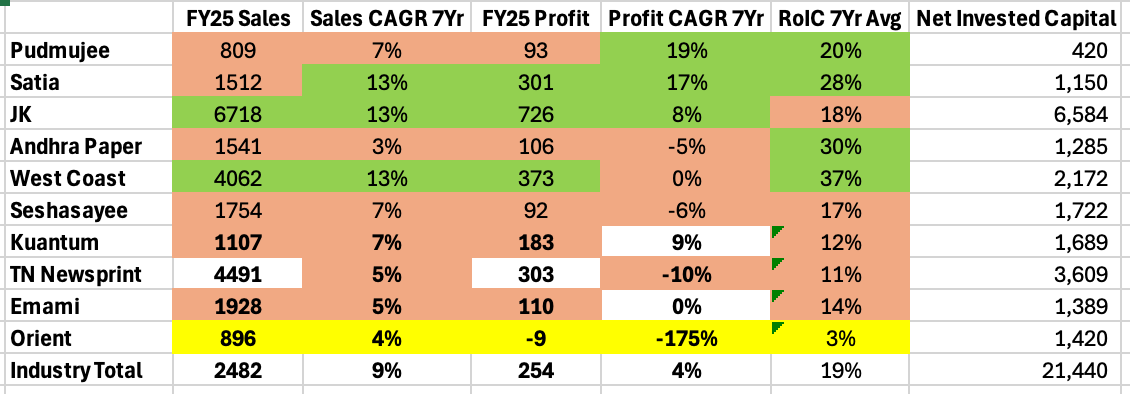

To illustrate this, I’m taking a deliberately simple, almost minimalist look at the Indian Paper Industry, focusing only on the major listed players: The Top 10 candidates by Market Capitalisation except ITC and Century Textile, two big giants as the Paper business only financials were not readily available (and I was being lazy).

The objective is not to build a forecasting model or build a stock specific thesis.

It is to listen to what the numbers and the narrative telling us about the industry.

What do the numbers tell us?

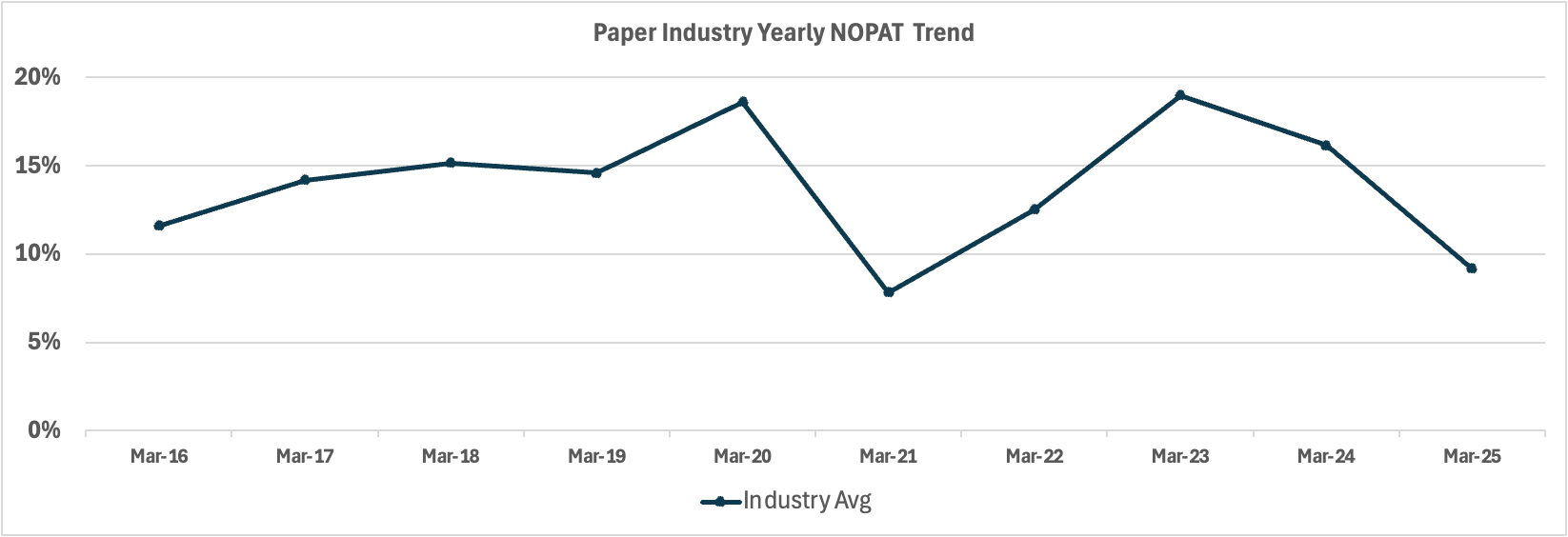

The Industry grew on average by 9% in revenue & 4%* profit in the last 7 Years

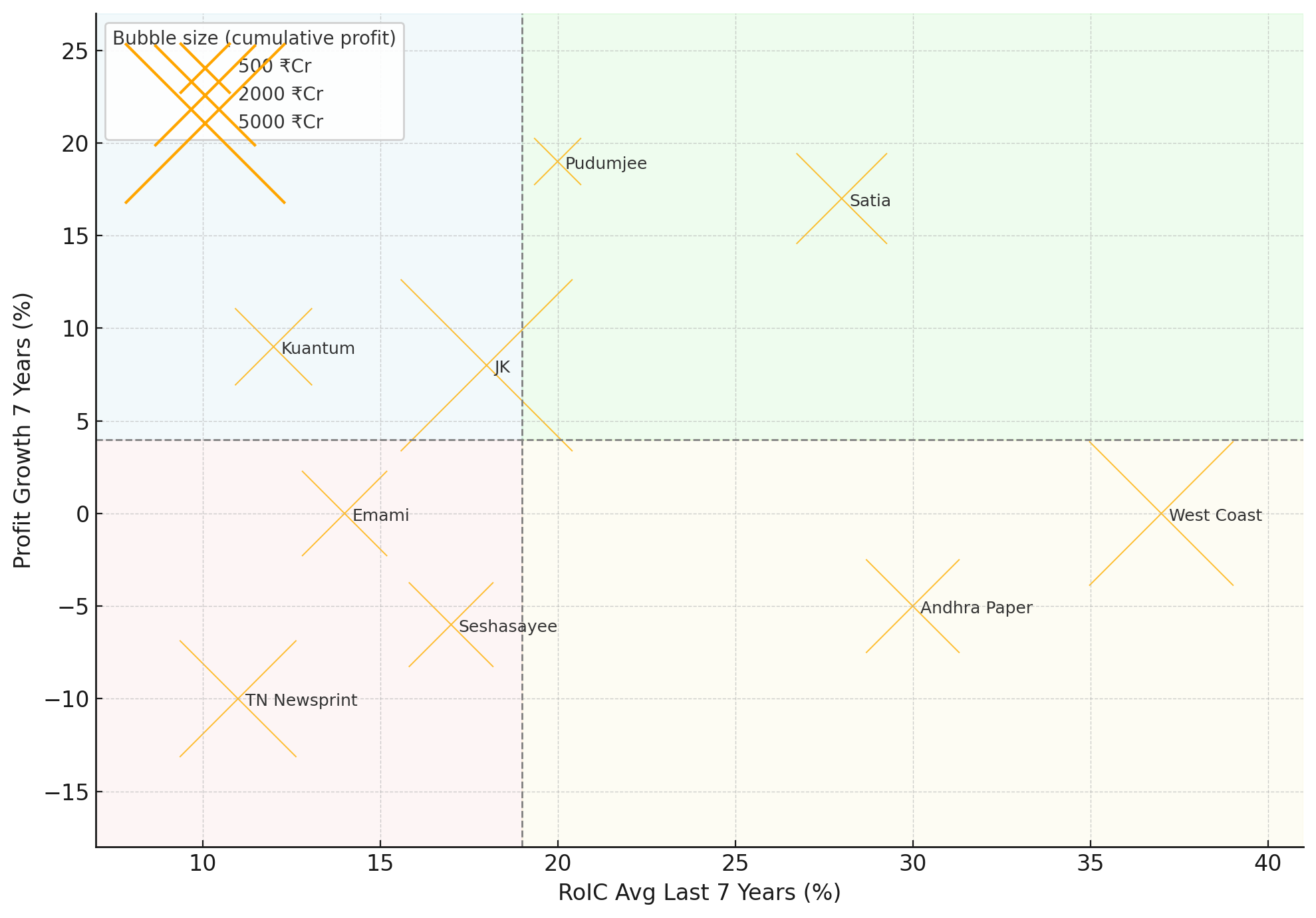

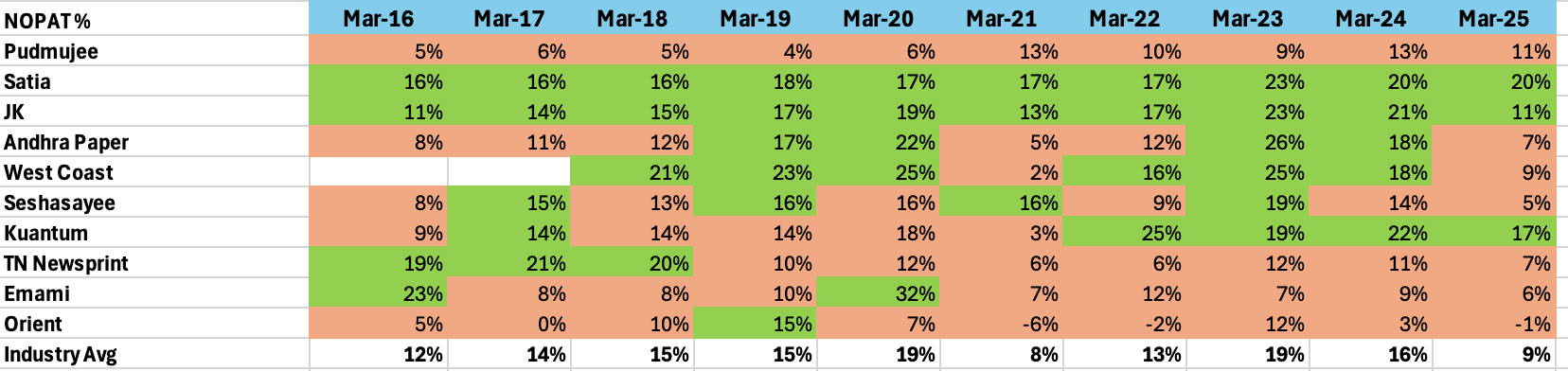

The majority of the players have decent Return on Invested Capital;

RoIC - Industry Average is a decent 19% - very good considering the almost commodity business

Seprating out outliers :- Secular double digit profit growth in a cyclical industry with high RoIC

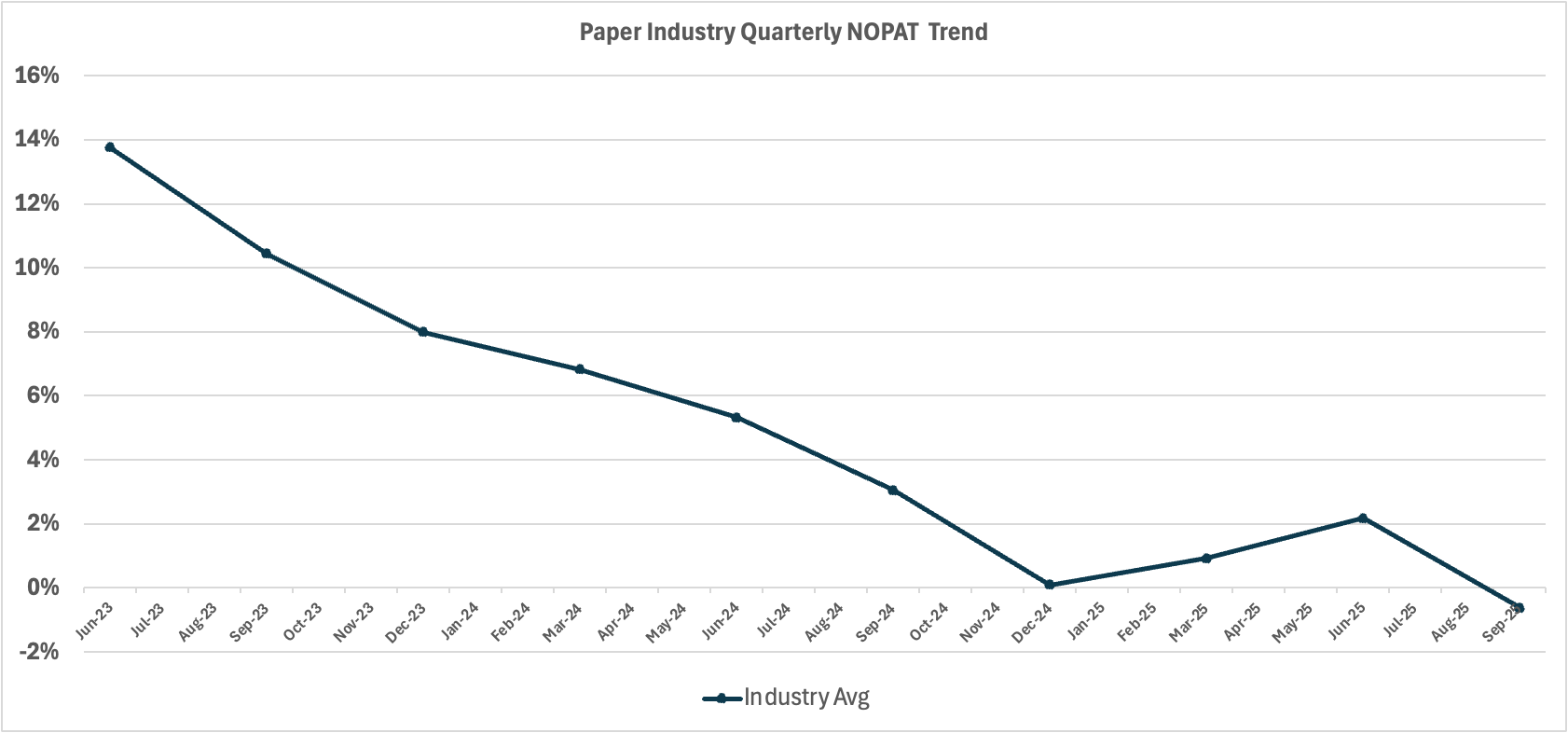

Industry is cyclical in nature; moves from negative to ~20% PAT margins every 3 years

Currently going through a downtrend in earnings due to lower realisations & RM increase

In any cycle, JK and Satia make more than Industry Average => Pricing Power=> Secular ?

The rest of the player`s profitability moves up and down along with overall market cycles

Something has drastically changed in Kuantum in last 3 years

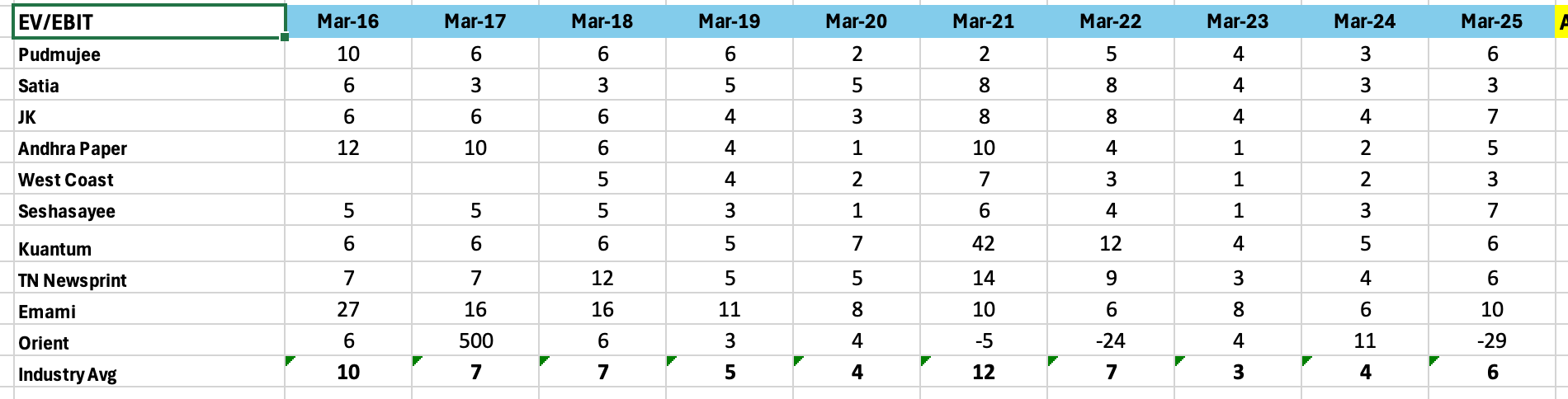

Industry valuations are 5 times EBIT on average*

What is the narrative of management from the Q2 results?

Mr. Chirag Satia, Satia Industry -

“ The Indian paper industry navigated a challenging quarter defined by elevated. input costs and depressed market realizations from persistent, low-priced imports.This was compounded by an inverted GST duty structure, increasing workingcapital and compressing near-term margins, an issue we are actively engaging policymakers to address.The revenue decline is attributed to temporary pressures, not a fundamental weakening in underlying demand, as we maintained stability through consistent production and strict cost discipline. The PM3 redevelopment has been deferred to ensure operational continuity, and early signs of easing wood prices, improved raw material availability, and lower fuel costs in the second half provide support for a gradual margin recovery " Mr. Harsh Pati Singhania, JK Paper -

“The Paper and Paper Board segment continue to face challenges arising from higher wood cost and lower sales realisation due to cheap imports. This has adversely impacted profitability across the product segments despite increased sales volume over the corresponding period.The performance of the Company’s packaging conversion subsidiaries improved during the quarter. Recent changes in GST rates have also had an adverse impact on the Paper & Board Industry. While GST on Paper and Boards has gone up from 12% to 18%, it has been reduced to 5% on converted products (Mono Cartons & Corrugated Boxes), resulting in inverted duty structure. In the case of Notebooks GST has become Nil, resulting in manufacturers in this sector being denied input credit. The disruption caused due to these GST changes has serious implications across the Paper and Board value chain, resulting in more expensive input costs for convertors, blockage of working capital, besides opening up the market to further cheap imports which do not have to bear the embedded taxes in domestic Paper and Board supplies. Representations have been made by Indian Paper Manufacturers Association (IPMA) and the converting industry regarding this anomaly to the Government and GST Council.”Mr. S K Bangur, West Coast Paper & Andhra Paper -

“The domestic paper industry continued to face pricing pressure through Q2 FY26 as imports remained elevated. Input costs, particularly wood, continue to remain high, moderating the pace of margin recovery. Further, consolidated performance is impacted during the quarter due to a brief workers’ strike and a subsequent 14-day planned annual maintenance shutdown at the Rajahmundry plant of one of our subsidiaries, Andhra Paper Limited, resulting in a one-time loss of production and earnings. Our company remain focused on strengthening our product mix, securing raw material supply, and driving cost efficiencies to sustain profitability."Mr. Gopalratnam, Seshasayee

“ The lower net profit in the current year was mainly due to:

- Lower average realisations per ton of paper.

- Significant drop in export sales volumes, particularly to US markets.

- Increase in the cost of wood, the key input material for the company.

Impacts from the above were partially negated by the overall reduction in the cost of production with better operations.

The Domestic Paper market continued to be sluggish in Q2 — FY 2025-26 due to poor order incoming amidst

- Disruptions caused by the GST 2.0 reforms announced by the Government in Q-2, where in the GST on Paper had got increased from 12% to 18%, affecting adversely the overall sentiments and order incoming.

- Imported Paper for Notebook conversion being made significantly cheaper with NIL GST or NIL GST ITC reversal, compared to domestically manufactured paper.

- Continued availability of imported paper at lower Prices.

- Few paper mills liquidating their inventory with deep discounts; thereby creating pricing pressures in the market.

- Disrupted supply chains globally due to the tariffs announced by US The international market for paper has not shown any signs of recovery and the drop in prices from Indonesia and China continue.So, what should we do?

Wait for one more quarter to see how the situation improves?

Completely leave this space, as too many variables?

Just trust the past numbers and buy the best players?

P.S. - My answer and My ChatGPT`s answer are the same :)

Also, a similar (not the same) situation had happened in the Egg Powder industry a year before, with both SKM Egg and Ovobel. It was too good to be true & simple to understand - and I missed it!

If you want to know more about the industry, then visit -

CARE Rating Report on Industry

Infomerics Report on the Indian Paper Industry

Energy & Geo-clusters mapping by BEE (Govt of India)

DISCLAIMER: I AM NOT A SEBI-REGISTERED ADVISOR OR A FINANCIAL ADVISOR. ALL THE VIEWS ARE FOR EDUCATIONAL PURPOSES. I MAY OR MAY NOT HAVE INVESTED IN THESE STOCKS. PLEASE DO YOUR DUE DILIGENCE YOURSELF. THIS IS NOT A STOCK RECOMMENDATION.

Great write-up. Any view on the specialty paper, like Pudumjee paper?