As a Marketing and Strategy guy, I can easily get lured into Loyalty Programs and Aggressive Branding efforts to promote. So when I came across Euro 7000 a White Glue brand sold by Jyoti Resins was doing something cool, and I wrote a post on it on my old WordPress, but it has been almost two years, and the revenue is flat , geographical expansion is slow and the stock price has corrected. So I thought of revisiting the Old Thesis with a bit of help from ChatGpt.

Old Post

Thanks for reading! Subscribe for free to receive new posts and support my work.

Cracking the CBJ right, the Euro 7000 way!

The Marketing Genius’ Jyoti Resins & Adhesives Ltd who makes Euro 7000 adhesive; in Direct Competition with Fevicol went right from 40-50 Rs in 2020 to 1500+ in 3 years. #Multibagger returns ! Small company from Gujrat with a visionary promoter who made a concentrated and a perfect bet ! Only to invest and invest fully into his ‘Consumer’ who is not us but the carpenter.

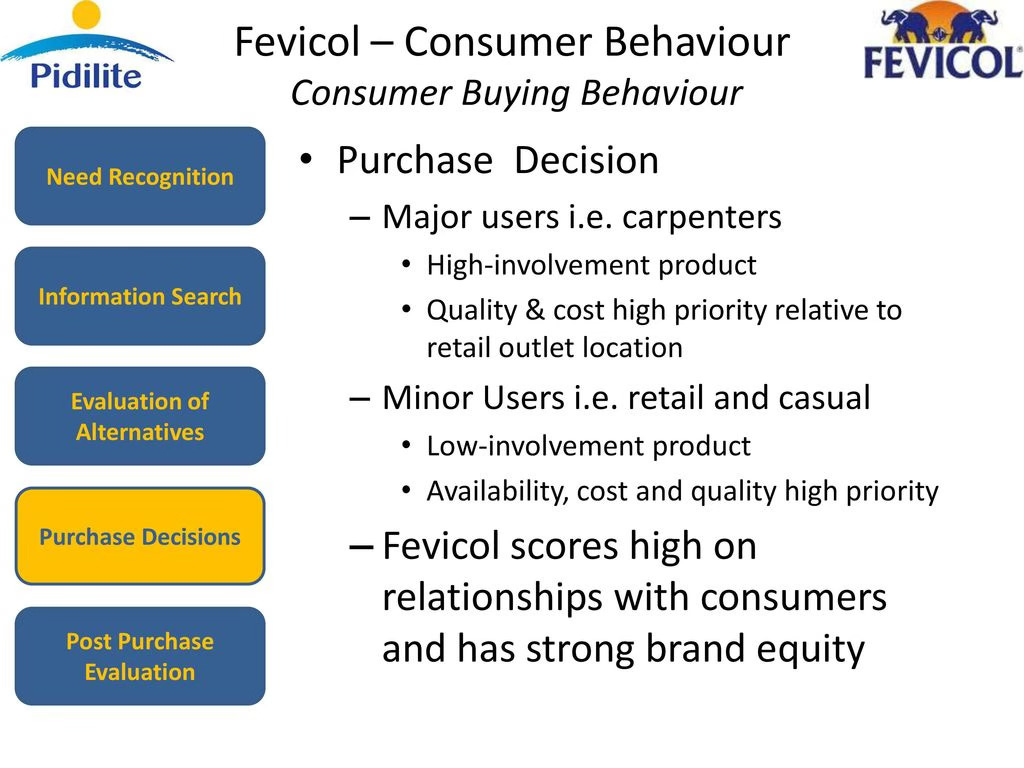

Look at the Consumer Buying Behavior made by some B school students (take it with a pinch of slot)

They cracked the #ConsumerBuyingJourney perfectly well. Their Carpenter Reward program worked like a charm. While Fevicol is an iconic brand, touching consumers through their memorable print and TV ads, Euro 7000 talks directly with the 3 lac carpenters through their mobile app, hardly any other marketing expense than this. What was the last time you had to do some interior/furniture work and asked your carpenter to buy only Fevicol because of the Brand Equity ? It is the carpenter who is an influencer and purchaser both. This creates an Exponential Pull, every referral and purchase creates a growth in demand and WTP.

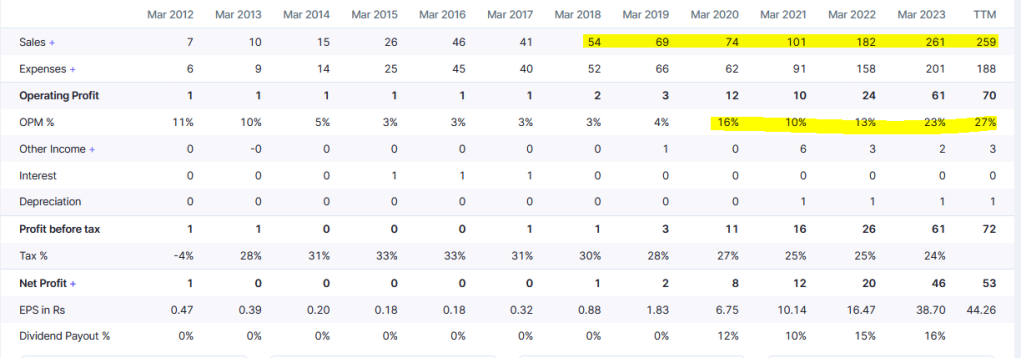

If we take a look at the financials, Revenue went up first, and then there is a huge margin expansion, indicating a strong Pull from the buyer/market.

As a Marketing Student, this is a delight and a rare sight. Cracking the Consumer Buying Journey sounds simple and yet it is very difficult. I think, the business is in still growth stage and has a good 3-5 year trajectory ahead. Good chances Adhesive space in Carpentry market would have become Duopolistic, need more on ground research to conclude that (there is Araldite and Loctite) . In the case of Duopoly, Euro 7000 will get bigger with every price increase that Fevicol takes, unless and until, Fevicol decides to undercut them.

Do you know any similar example of getting the CBJ right ? Apple isnt the only answer !

New Post:

From Loyalty to Leverage: Inside Jyoti Resins' Marketing Flywheel

The Shift: From Push to Pull

Until recently, Jyoti Resins was largely a push-driven operation: get stock to retailers, nudge sales through dealer schemes, and layer on loyalty points for carpenters. It worked well enough to reach ~₹284 Cr in revenue by FY25. But FY23 and FY24 exposed cracks in this model. Volume stalled. ASP peaked. And the company faced a classic B2C challenge: how do you scale beyond a trade network without losing your margins?

Enter the Marketing Flywheel

In FY25, management started laying the foundations of a flywheel.

Three moves stand out:

Elevating the Brand: The appointment of Pankaj Tripathi as brand ambassador was more than celebrity endorsement. It was a signal: Euro 7000 wants mindshare, not just shelf space.

Budget Realignment: Marketing and branding expenses will now move from ~2% of sales to a planned 7-8%, with a 50-50 split between trade and consumer spends. This is strategic rebalancing.

Loyalty Tech Stack: The carpenter app isn’t just a points ledger anymore. It's a data platform -one that can eventually inform geo-activation, product mix, and even NPS.

Is the Loyalty Program working?

Here's how the numbers stack up:

Notice the trend.. behind every Crore spent on loyalty program, the volume has come down from 3.4 Cr revenue per crore spent to 3 Cr revenue now on average in FY24 and FY25, volumes sold per crore spent on loyalty has come down from ~260 Tonnes to ~130 Tonnes (and mind you capacity of the plant is not a problem), indicating diminishing marginal returns. But FY25's slight rebound in branding efficiency hints that the pivot to B2C branding may be working.

Another way of looking at this is that now the marketing team knows that they don’t have to spend more than ~100 Cr to get ~300 Cr of Topline !! If we assume this as a linear relationship going ahead, then for Euro7000 to match Fevicol topline of 11500 Cr; they will have to spend ~3500 Cr in Loyalty Program! <Haha>

This is a joke. Pidilite spends ~1000 Cr in branding/marketing. Also most of the relationships in life are not linear :)

Loyalty Also Needs to be Paid :p

Here's the hard part. Jyoti Resins is sitting on a ₹95 Cr liability in its books—carpenter loyalty points yet to be redeemed. Of that, 80% is carpenter-focused, with the rest going to dealer schemes and appliances. And while it's deferred on the balance sheet, there's no expiry date. Redemption risk is real.

To address this, the company has:

Kept Cash and Cash Equivalents of ~150 Cr

Hired 200+ staff to support the loyalty ops engine

Built a redemption app and depot pickup model

Created CRM touchpoints for proactive redemption nudges

Still, until redemption accelerates or terms evolve, this loyalty corpus could remain a latent P&L overhang. Also, the Efficiency of this program is still a question for me.

What Lies Ahead

With 48 branches, 12,500+ retailers, and 3.5 lakh carpenters on board, Jyoti Resins has reached a strategic inflexion. If it cracks the marketing flywheel, the brand can scale from loyalty-driven margins to pricing power and customer pull.

The question is no longer "Can they sell more adhesive?" The question now is: "Can they build Euro 7000 into the Fevicol of the next decade—without Fevicol's ad budget?"If you ask me, they've made a gutsy start.

Disclosure: This post is not investment advice. It reflects a marketing strategist’s lens on an emerging brand story. Data sourced from company annual reports, conference calls, and investor presentations. Some of the numbers are assumed or derived.

DISCLAIMER: I AM NOT A SEBI-REGISTERED ADVISOR OR A FINANCIAL ADVISER. ALL THE VIEWS ARE FOR EDUCATIONAL PURPOSES. I MAY OR MAY NOT HAVE INVESTED IN THESE STOCKS. PLEASE DO YOUR DUE DILIGENCE YOURSELF. THIS IS NOT A STOCK RECOMMENDATION.

Thanks for reading! Subscribe for free to receive new posts and support my work.

The Loyalty program provision should typically be a closing figure. Does the PnL have an actual expenses for this? That should be used for division. Some may actually have redeemed the loyalty program points.

Also, secondly how effectively are these rewards also matters in the perspective of the carpenter.

For all we know, say even if 50 percent of these rewards can't be redeemed then the company may just end up spending half of this and it may not be as smart a move and lead to negative publicity in terms of not being of great use in the carpenter word of mouth community.

The Loyalty program provision should typically be a closing figure. Does the PnL have an actual expenses for this? That should be used for division. Some may actually have redeemed the loyalty program points.

Also, secondly how effectively are these rewards also matters in the perspective of the carpenter.

For all we know, say even if 50 percent of these rewards can't be redeemed then the company may just end up spending half of this and it may not be as smart a move and lead to negative publicity in terms of not being of great use in the carpenter word of mouth community.

Super analysis. Buy?